Cv Mat Variance

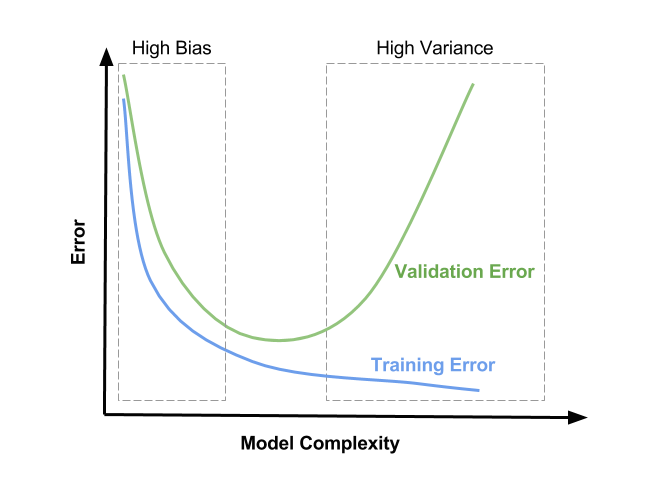

Variance Learn Opencv

Detect Blurry Images With Laplacian Variance Issue 448 Justadudewhohacks Opencv4nodejs Github

How To Calculate Variances Sv Schedule Variance Cv Cost Variance Spi Project Management Professional Earned Value Management Small Business Management

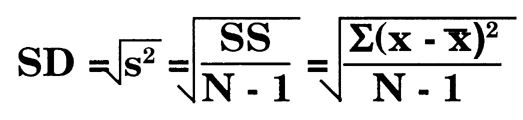

Standard Deviation Formula Standard Deviation Earned Value Management Formula

10 Ways To Present Variance Analysis Reports In Excel Free Excel Tutorials Tips Tricks Techniques Dashboard Tem Excel Tutorials Excel Formula Resume Tips

Area Under The Curve Auc And Variance Estimates Calculated With Two Download Scientific Diagram

The function ignores nans.

Cv mat variance.

Cost Variance Formula In 2020 Earned Value Management Cost Accounting Analysis

Z 5 Sum Of Squares Variance And The Standard Error Of The Mean Westgard

Opencv Cv Img Hash Radialvariancehash Class Reference

What S The Theory Behind Computing Variance Of An Image Stack Overflow

Poster Designs Color Design Typography Theory Con Imagenes Tipografia Disenos De Unas Diseno Grafico

Mean Variance Coefficient Of Skewness And Excess Kurtosis For The Download Table

Combined Analysis Of Variance Mean Square For Effect Of Pruning And Download Table

Variance Analysis In Excel Making Better Budget Vs Actual Charts Pakaccountants Com Microsoft Excel Tutorial Excel Tutorials Microsoft Excel Formulas

A Sample Income Statement Modified For Budget Variance Analysis Income Statement Financial Analysis Cost Accounting

Click Here To Download This Financial Analyst Resume Template Http Www Resumetemplates101 Com Fina Business Analyst Resume Business Analyst Executive Resume

Pdf Can Analysis Of Variance Be More Significant

Coefficient Of Variance Cv Of Common Size Items Download Table

Cover Letter Template Accounting Accounting Cover Coverlettertemplate Letter Tem Cover Letter Example Job Cover Letter Examples Cover Letter For Resume

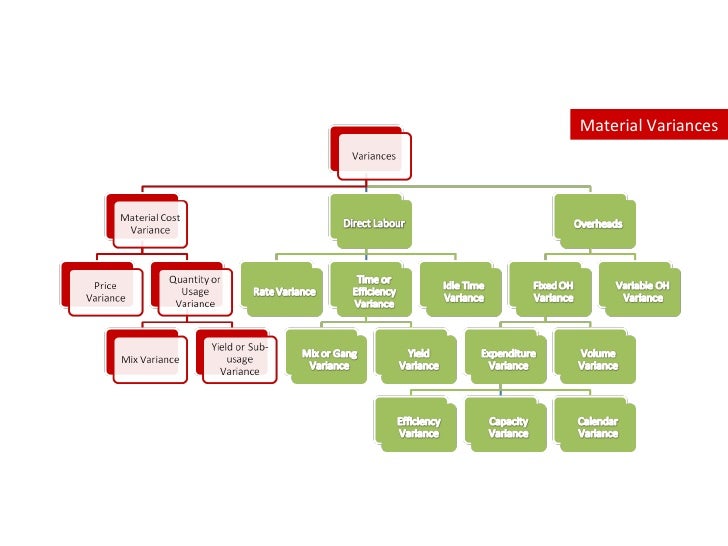

Variance Analysis

6 Of The Best Gantt Chart Software Gantt Chart Investment Services Gantt

Factor Loadings And Proportion Of Variance Explained By Each Domain For Download Table

Pdf Estimation Of Quantal Size And Number Of Functional Active Zones At The Calyx Of Held Synapse By Nonstationary Epsc Variance Analysis

Pdf Five Project Duration Control Methods In Time Units Case Study Of A Linearly Distributed Planned Value

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcs8xe52shj2jpovgcfgprlynaspmrqmndhoje41ozpxyuifal9l Usqp Cau

Pdf Linear Transformations Of Variance Covariance Matrices

Partitioning Of The Nested Variance In Eight Functional Traits Measured Download Scientific Diagram

Pdf Adding Bias To Reduce Variance In Psychological Results A Tutorial On Penalized Regression

I Love Month End Funny Accounting Quote Mouse Mat Zazzle Co Uk Funny Accounting Quotes Accountability Quotes Love Month

Vertical Actual Vs Target Charts In Excel Top To Bottom Variance Analysis Using Bar Charts Excel Tutorials Excel Excel Hacks

Source : pinterest.com